%20Website%20Logo%20(Veguilla%20Law%20Firm%20PLLC)%20FINAL%20(compressed).png)

What is Bankruptcy?

BANKRUPTCY

Bankruptcy is a judicial process provided by federal law to help debtors, whether individuals or businesses, eliminate their debts or repay them, protected by the guarantees provided by the bankruptcy court. Bankruptcy law, in a nutshell, seeks to rehabilitate the debtor and allow him to start his financial life anew, free of the debts that can weigh him down.

People primarily turn to bankruptcy protection because they face unforeseen medical expenses, excessive credit card debt, job loss, and divorce. These events, apart from being stressful and sometimes traumatic experiences, also bring economic difficulties. There are different alternatives to deal with these situations, and we are more than willing to explore them with you before considering whether bankruptcy is right for you.

The Bankruptcy Code provides different mechanisms for different types of debtors, these mechanisms are identified by the specific chapter of the Bankruptcy Code that regulates them.

Chapter 7 (Liquidation)

This type of bankruptcy is known as liquidation, because as part of this process the debtor delivers to a Chapter 7 Trustee, all his assets not protected by the Code, so that they can be liquidated, that is, they are sold by the Trustee, who in turn distributes the money obtained from the sale to the debtor's creditors. The benefit that debtor receives in this process is a discharge of his debts. Discharge is the term used to describe the bankruptcy court's power to forgive a debtor's debts. Once the discharge is granted, all the debts that the Code allows are eliminated by the court, and cannot be collected, it does not matter if the assets of the debtor were not sufficient to pay all the debts. Another very important benefit of this and other bankruptcy mechanisms is the immediate cessation of all claims and collection proceedings, at the time the bankruptcy petition is filed.

You could benefit from a Chapter 7 bankruptcy filing if your debts are greater than the value of the assets you own. An additional advantage to you in a Chapter 7 filing is that the bankruptcy case is filed fairly quickly, being able to receive a discharge 3-4 months after filing.

Chapter 13 (Plan)

This type of bankruptcy has the characteristic of allowing the debtor to pay part of his debts through a payment plan, within a period of 3 to 5 years. Chapter 13 allows the debtor to keep assets that he or she otherwise would have had to turn over to the trustee in a Chapter 7. In addition, this chapter allows the stay of collection efforts to benefit not only the debtor filing for bankruptcy, but codebtors as well, such as joint guarantors and co-signers in a loan. You may benefit from a Chapter 13 bankruptcy if you have a regular source of income, but your income is not enough to meet all the required monthly payments to your creditors. You could also benefit from a Chapter 13 bankruptcy if you own your residence, and it is worth more than you owe on it (you have equity). Under Chapter 13 you could also protect loved ones, such as your parents or siblings, who have co-signed on a debt of yours, and which you can no longer pay as originally contracted. In this way, your relatives would not have to answer to your creditors, for the duration of the Chapter 13 payment plan, for debts you include in your bankruptcy petition in which they are co-debtors..

The Automatic Stay

One of the most important advantages for a debtor who files for bankruptcy is the automatic stay of all collection efforts against him and his assets. The stay is automatic since it is not necessary for the bankruptcy judge to issue any particular order, since it enters into effect upon the filing of the bankruptcy case. Once the stay is in effect, many of the most common collection efforts are prohibited, and any creditor who violates the stay is exposed to sanctions. In addition, those actions that are carried out while the stay is in effect and which run afoul of it can be annulled by the bankruptcy court. The debtor whose wages had been garnished for the payment of debts will benefit to the extent that said garnishment must stop immediately after filing for bankruptcy. Even lawsuits against the debtor pending in other courts are paralyzed by the filing of a bankruptcy petition.

The main purpose of the stay is not eliminate debts permanently, but to provide the debtor with a breathing space, so that he can concentrate on his bankruptcy case and resolve his debts, without being overwhelmed by the innumerable demands of creditors.

.jpg)

How can the stay help me stop a collection lawsuit?

Many people find out that a creditor has filed a collection lawsuit when they receive the citation for said lawsuit. The citation informs you of your opportunity to file an answer to the lawsuit. If you file an answer, the court will schedule either a trial or a pre-trial hearing to discuss any issues, such as witnesses to be called at trial. If you do not answer the lawsuit, the court may deem the allegations in the lawsuit as admitted and proceed to issue a default judgment against you without giving you any further notice.

The filing of a bankruptcy activates the automatic stay provided for in the Bankruptcy Code, and therefore any trial or pre-trial hearing cannot be held, since it is part a creditor’s efforts to collect a debt against you.

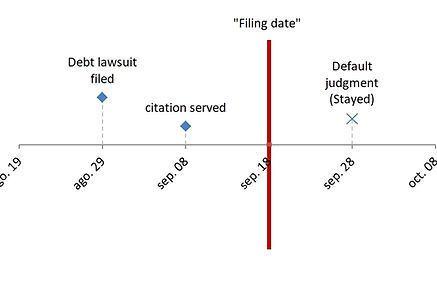

In this example, the debtor received the citation on September 8 for the lawsuit filed on August 29. When the debtor files his bankruptcy on September 18 (the "Filing Date"), the deadline to answer the lawsuit before September 22 is stayed. If the plaintiff, already aware of the debtor's bankruptcy, insists on their collection efforts or tries to induce the Court to issue a default judgment regardless, they will be in clear violation of the Bankruptcy Code and may face sanctions from the Bankruptcy Court. Additionally, any judgment obtained by the plaintiff after the bankruptcy petition can be annulled by the Bankruptcy Court.

How can the stay help me stop the repossession of my car?

The bank or company that lent the money for the purchase of the car, which serves as collateral for the payment of that debt, can repossess the vehicle if there's a delay in payments. When this happens, the creditor will contact the debtor to inform them that they will repossess the vehicle. Once the debtor files for bankruptcy, the creditor has to halt all collection efforts, including the process of repossessing the car.

.jpg)

In this example, the debtor receives a call from the creditor on July 15, indicating that they will repossess the car due to non-payment. Once the debtor files their bankruptcy on July 17, the bank is obligated to halt all collection efforts, including the attempt to repossess the car on July 19, as previously planned. If the creditor, knowing about the debtor's bankruptcy, insists on their collection efforts and repossesses the vehicle on July 19, they will be in violation of the Bankruptcy Law, may be subject to sanctions, and the Bankruptcy Court can order them to return the car to the debtor.

How can the stay help me stop wage garnishment?

Certain creditors with debts such as unpaid federal taxes, federal student loans, child support, and spousal maintenance have the legal authority to garnish part of the wages of those who owe them money and have not reached any payment arrangement. Wage garnishments are also prohibited collection efforts when the debtor files for bankruptcy.

In this example, the debtor's paychecks dated March 30 and April 15 have been subject to garnishment. Once the debtor files for bankruptcy on April 23, all subsequent paychecks must be received in full—that is, without any money being deducted for garnishment. If, due to error or lack of knowledge, the debtor's employer withholds additional funds after the bankruptcy has been filed—whether the employer or the creditor (if the latter has already received the funds)—they may be ordered to return those funds to the debtor.

What are exemptions and how do they help me?

Every debtor has the right to keep certain assets, even if they are the subject of a judicial process seeking to seize their property for the payment of a debt. All states have various legislations to protect all kinds of debtor assets from the hands of creditors. This body of laws that provide this type of protection to a debtor is known as exemptions. The differences between allowed exemptions between one jurisdiction and another can be quite significant.

The Bankruptcy Code provides its own list of exemptions, which, along with other federal laws, are known as federal exemptions. These federal exemptions can be invoked instead of the local exemptions of the debtor's state of residence.

Exemptions allow the debtor to retain most if not all of their assets, even when going through a bankruptcy process. This way, the debtor is not condemned to a state of helplessness, and they are given the means to rehabilitate their finances without having to start from scratch.

How can the homestead exemption help me protect my house?

The homestead exemption is the name given to the exemption provided by law to protect a debtor's home from having to be used to satisfy debts, except for those such as voluntary mortgages on the home. The Bankruptcy Code provides a fixed maximum amount of money that can be claimed against the equity of the house. To understand how to calculate the protection provided by the homestead exemption, it is necessary first to determine the value of the house.

For the purpose of this example, let's assume the house is valued at $100,000. Secondly, it's necessary to determine how much of the house's value is committed to securing a mortgage loan, if any.

Let's assume the house has a mortgage balance of $80,000. The mortgage creditor has greater protections than a creditor holding a personal debt, as they have the right to sell the collateral (the house) to satisfy their claim before other creditors. As we can see in this example, if this house was sold and the mortgage paid off, there would be approximately $20,000 of equity remaining. This equity is the amount of money available for paying other debts, such as personal debts (credit cards, loans, and others). The Chapter 7 trustee can use this equity to pay off those debts, unless the debtor uses an exemption.

In this example, we'll use the amount of $22,000 as the total exemption allowed by bankruptcy law for the value of a house (this is an approximation; the actual amount is subject to additional considerations and periodic revisions). Since the house secures a mortgage loan with a balance of $80,000, the exemption only applies to the property's equity. Therefore, we have enough exemption money to protect the entirety of the $20,000 equity in this house, leaving a surplus of $2,000 exemption that we didn't have to use.

Once this exemption is claimed on the entire equity of the house, that equity, and therefore the house itself, is protected from liquidation by the Chapter 7 trustee.

There are also other exemptions in Bankruptcy Code that apply to other assets such as vehicles, household furnishings, money accumulated in retirement accounts, and others.

This is a fairly simplified example of how exemptions are used in the context of a bankruptcy case. The proper and precise application of exemptions requires more analysis than what this brief example allows for. Bankruptcy court decisions also interpret and modify the way these calculations are carried out. Nothing replaces the advice of a bankruptcy attorney to help you understand how you can benefit from exemptions in a bankruptcy case.

¿How can Bankruptcy help me keep my car?

A person who has a financed car may fall behind on their payments and find themselves in a situation where the creditor who lent the money for the car tries to repossess it.

In bankruptcy, there are several ways in which a debtor can remedy these defaults and keep their vehicle, as explained below:

Pay the arrears through bankruptcy.

In this alternative, the debtor can file a Chapter 13 bankruptcy, and as part of their payment plan, arrange for the payment of any arrears on their car loan. For example, if a debtor fell behind on payments due on January 1, February 1, and March 1 and files for bankruptcy on March 25, they could pay these three months as part of their bankruptcy plan. This will allow them more time to catch up on these arrears (up to 5 years). As for the current payments due on April 1 and subsequent payments, the debtor can continue making payments directly to the creditor. When these current payments are received, the creditor is required to credit them to the corresponding months and cannot apply them to the past-due months.

Pay off the entire debt through bankruptcy

In this alternative, the debtor can decide to pay not only the arrears but the entire principal balance through their Chapter 13 bankruptcy. This may mean that instead of having to continue paying high monthly payments, the debtor can extend the term of the original loan (up to 5 years) and thereby reduce the amount they have to pay each month.

Pay the value of the vehicle only.

In some circumstances, if certain requirements are met, the debtor can propose in their Chapter 13 payment plan to pay the creditor the value of the car in the market at the time of filing, rather than the balance of the debt. This option makes sense as cars typically depreciate rapidly. Therefore, the majority of vehicles are worth much less than what is still owed to the creditor.

In addition to these alternatives, a Chapter 13 can also be useful for reclaiming a vehicle that has recently been repossessed by the creditor. Once bankruptcy is filed, if the vehicle has not yet been sold at auction, it is the creditor's obligation to return it to the debtor, so that the debtor can catch up on any arrears through their payment plan.

How can Bankruptcy help me save my home from foreclosure?

At times, you may fall behind on one or two mortgage payments, and it will likely be nearly impossible for you to catch up on them all at once. You, like many other debtors, typically continue making scheduled mortgage payments as months go by, but since you already have months of arrears, the bank doesn't use that money to credit the current month but the oldest overdue month. At this rate, you are not making current payments, as all your payments are going towards covering the arrears. The bank will eventually stop accepting additional payments from you until you catch up on all arrears and the current payment. With this unilateral decision by the bank, you will quickly fall into major default, as more months of arrears accumulate, even if you have been willing to keep making payments. Sooner than you expect, the bank will sue you for foreclosure.

Filing a Chapter 13 bankruptcy can be your tool to bring your loan current without needing to pay off the entire arrears all at once and to force the bank to accept the current mortgage payments, so the arrears don't keep growing.

.jpg)

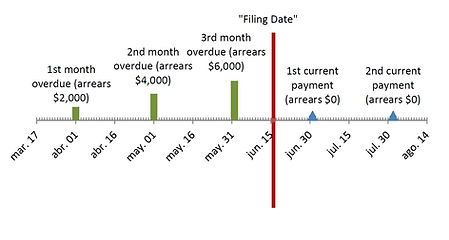

In this example, let's assume your mortgage payment is $2,000. You already behind on the payments for April and May , and by June, the bank refuses to accept a payment of only $2,000. The bank will only accept $6,000 (the two overdue months plus the current month) or they won't accept any payment at all. Once you file for bankruptcy under Chapter 13, the bank is prohibited from taking this position. The bank is obligated not only to receive the payment for July but also to credit it to the month of July.

The Bankruptcy Law prevents the bank from using the money you pay them monthly after the filing to cover the pre-petition arrears. These pre-petition arrears can be paid through your Chapter 13 plan, in a period that can be up to five years. During the life of the Chapter 13 plan, as long as you comply with both the current mortgage payment and the Plan payment, your mortgage loan will be considered current for purposes of interest on late charges. The bank cannot initiate any foreclosure action. By the end of your bankruptcy, you will have covered the pre-petition arrears, and the bank will have received the current payments after the filing. Therefore, at the conclusion of your bankruptcy, your mortgage loan will be current again.

¿What is the Texas Homestead Law, and how does it protect my property?

Apart from the federal exemptions provided by the Bankruptcy Code, Texas also provides a series of state exemptions to protect debtor’s property from the seizure by creditors. Provided by the Texas Constitution, as well as the Texas Property Code, Texans can claim interest in land and in personal property.

In the case of land, while the is no limit to the value of the property to be exempted, the land in question can be:

- Up to 10 acres of land, if used for purposes of an urban home, or both an urban home and a place of business, for the use of a family or a single adult person.

- Up to 200 acres of land, if used for purposes of a rural home, for the use of a family or a single adult person.

In the case of personal property, there is an aggregate limit of $50,000 for personal property of an individual, or $100,000 for personal property of a family. And the personal property to be exempted can include:

(1) home furnishings, including family heirlooms;

(2) provisions for consumption;

(3) farming or ranching vehicles and implements;

(4) tools, equipment, books, and apparatus, including boats and motor vehicles used in a trade or profession;

(5) wearing apparel;

(6) jewelry (not to exceed 25 % of either the $50,000 or $100,000 limit;

(7) two firearms;

(8) athletic and sporting equipment, including bicycles;

(9) a two-wheeled, three-wheeled, or four-wheeled motor vehicle for each member of a family or single adult who holds a driver's license or who does not hold a driver's license but who relies on another person to operate the vehicle for the benefit of the nonlicensed person;

(10) the following animals and forage on hand for their consumption:

(A) two horses, mules, or donkeys and a saddle, blanket, and bridle for each;

(B) 12 head of cattle;

(C) 60 head of other types of livestock; and

(D) 120 fowl; and

(11) household pets.

How can I dispute a debt in the bankruptcy process?

One of the major advantages of bankruptcy is that the debtor is not obligated to pay the entirety of the most common debts, such as personal loans and credit cards. This is because, in the case of these debts (called "unsecured non-priority debts"), the Bankruptcy Code is more concerned with whether the debtor can pay or not, and how much the debtor can reasonably contribute to the payment of these debts, rather than focusing on the total balance of each debt. In other cases, it is required that the debtor pay the total balance of certain debts ("priority debts") or at least bring any arrears up to date ("secured debts").

However, this doesn't mean that the debtor has to accept the creditor's claim of the debt balance.

As part of the bankruptcy process, any creditor who wishes to receive payment from the trustee, whether in Chapter 7 or 13, must submit a proof of claim to the court. In this document, under oath, the creditor assures the court that they indeed own a claim against the debtor, describes the nature of the debt, the balance of the debt as of the filing date, and any evidence necessary to support its validity.

If the debtor disagrees with any of these creditor allegations in their proof of claim, they can file an objection to the claim and bring to the court's attention any arguments or evidence that refute the alleged debt. Things that can be objected to include: the debt balance, the existence of the debt, the debtor's responsibility to pay it.

In the normal course of life, when you have a disagreement with a creditor about whether a payment was made correctly or not, it is very difficult or almost impossible to get the creditor to admit an error and agree with you. The creditor holds all the cards, and in most cases, the creditor's version prevails, not because they are right, but because they are the stronger party in the transaction.

The bankruptcy process provides the debtor with a more equitable space in which to air these disputes, which will ultimately be resolved by a judge, rather than the whim of the creditor.

Only after this dispute is resolved, and the correct amount of the debt is determined, as the case may be, can payment be provided, either in full or in part, or the discharge of the entire balance.

This process of objecting to the creditor's claim is available to challenge all types of debt, including federal and state taxes, fines, utilities, rent contracts, and many others.

Add to this the benefit of automatic stay, which prohibits the creditor from continuing collection efforts while bankruptcy is pending, and you can understand why it is much more favorable for you to fight for your rights in the bankruptcy forum than directly with the creditor.